Every year, salaried people in India face the same confusion.

Should you choose the new tax regime or stick with the old one?

And most people don’t actually calculate both. They just follow what someone at work said or assume the old regime must be better because it allows deductions.

That’s lazy — and expensive.

So let’s break down New vs Old Tax Regime 2026 properly using official FY 2026–27 slabs and real salary examples.

If you ever want to cross-verify slab rates or notifications, you can check the official Income Tax India e-Filing Portal.

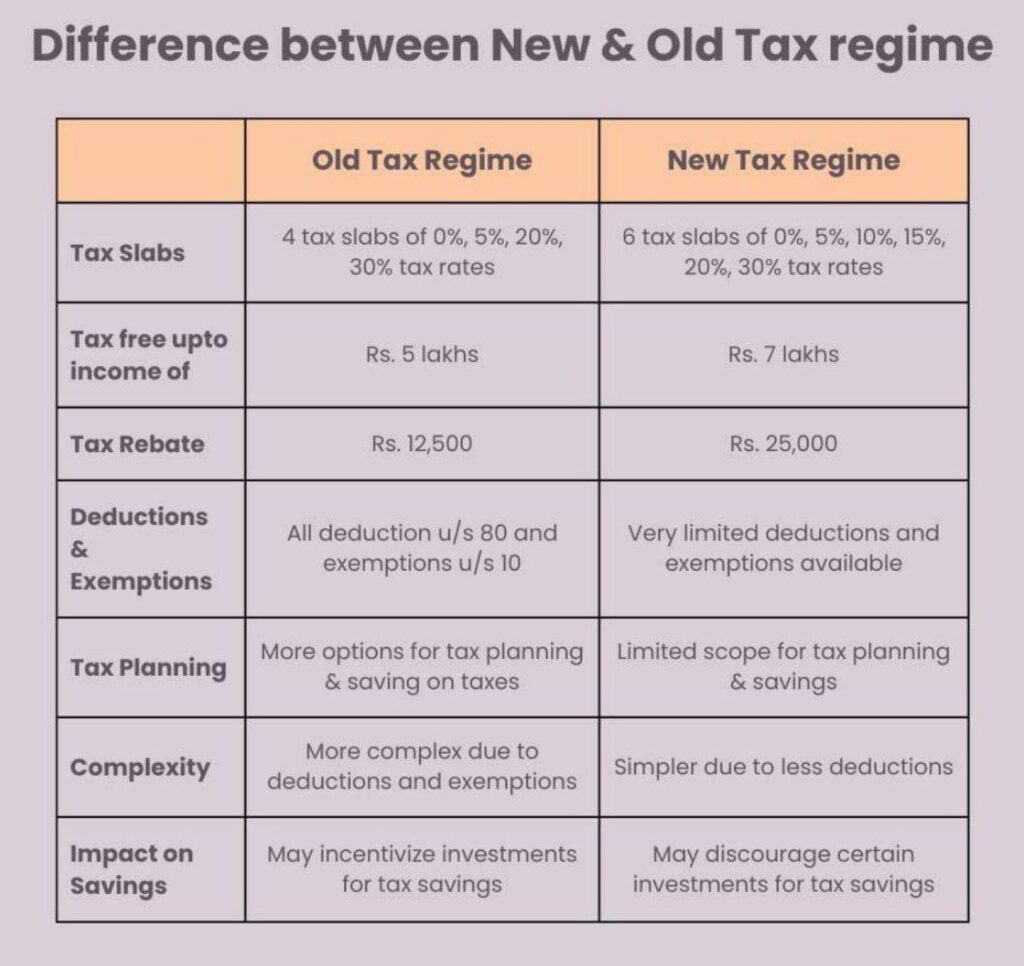

First, Understand the Core Difference

Before jumping into numbers, here’s what actually separates the two regimes.

New Tax Regime 2026

- Lower tax slab rates

- Standard deduction of ₹50,000 for salaried employees

- Very limited deductions

- Section 87A rebate if taxable income is up to ₹12 lakh

- 4% Health & Education Cess applies

The government has been encouraging this regime in recent budgets presented by Nirmala Sitharaman, and official announcements are available on the Union Budget portal.

The idea is simple: lower rates, fewer complications.

Old Tax Regime

- Higher tax slab rates

- Allows deductions like:

- Section 80C (₹1.5 lakh limit)

- Section 80D (health insurance)

- HRA

- Home loan interest (Section 24)

- LTA and others

You can verify available deductions on the official Income Tax Deductions & Exemptions page.

Old regime rewards planning. But you need proper documentation.

Now let’s stop theory and calculate.

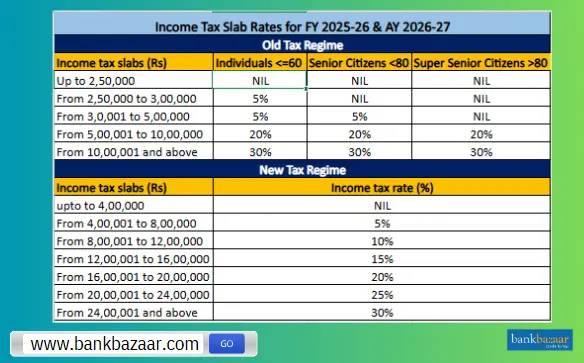

Salary Scenario 1: ₹7 Lakh Per Year

Let’s assume a salaried employee earning ₹7,00,000 annually.

Under New Tax Regime 2026

Gross income = ₹7,00,000

Standard deduction = ₹50,000

Taxable income = ₹6,50,000

Tax Calculation

- ₹0 – ₹4L → 0

- ₹4L – ₹6.5L (₹2.5L at 5%) → ₹12,500

Total tax = ₹12,500

Cess (4%) = ₹500

Total before rebate = ₹13,000

Since taxable income is below ₹12 lakh, Section 87A rebate applies.

Final tax payable = ₹0

Under Old Tax Regime (No Deductions Claimed)

Taxable income = ₹6,50,000

- ₹0 – ₹2.5L → 0

- ₹2.5L – ₹5L → ₹12,500

- ₹5L – ₹6.5L (₹1.5L at 20%) → ₹30,000

Total tax = ₹42,500

Cess (4%) = ₹1,700

Final tax payable = ₹44,200

Verdict at ₹7L

Under New vs Old Tax Regime 2026, the new regime clearly wins at ₹7 lakh.

Unless you have serious deductions, choosing old regime here makes no financial sense.

Salary Scenario 2: ₹10 Lakh Per Year

This is where most salaried professionals fall.

Annual income = ₹10,00,000

Under New Tax Regime 2026

Gross income = ₹10,00,000

Standard deduction = ₹50,000

Taxable income = ₹9,50,000

Tax calculation:

- ₹0 – ₹4L → 0

- ₹4L – ₹8L → ₹20,000

- ₹8L – ₹9.5L (₹1.5L at 10%) → ₹15,000

Total tax = ₹35,000

Cess (4%) = ₹1,400

Total before rebate = ₹36,400

Taxable income under ₹12L → rebate applies

Final tax payable = ₹0

Under Old Tax Regime (With Basic Deductions)

Assume:

- ₹1.5L under 80C

- ₹25K under 80D

Total deductions = ₹1,75,000

Taxable income = ₹8,25,000

Tax calculation:

- ₹0 – ₹2.5L → 0

- ₹2.5L – ₹5L → ₹12,500

- ₹5L – ₹8.25L → ₹65,000

Total tax = ₹77,500

Cess (4%) = ₹3,100

Final tax payable = ₹80,600

Verdict at ₹10L

New regime = ₹0

Old regime = ₹80,600

That’s not a small gap.

For most salaried individuals at ₹10L, the new regime is financially stronger in 2026.

Salary Scenario 3: ₹15 Lakh Per Year

Now let’s move higher.

Annual income = ₹15,00,000

Under New Tax Regime 2026

Gross income = ₹15,00,000

Standard deduction = ₹50,000

Taxable income = ₹14,50,000

Tax calculation:

- ₹0 – ₹4L → 0

- ₹4L – ₹8L → ₹20,000

- ₹8L – ₹12L → ₹40,000

- ₹12L – ₹14.5L (₹2.5L at 15%) → ₹37,500

Total tax = ₹97,500

Cess (4%) = ₹3,900

Final tax payable = ₹1,01,400

Rebate does not apply (income above ₹12L).

Under Old Tax Regime (With Strong Deductions)

Assume:

- ₹1.5L under 80C

- ₹25K under 80D

- ₹2L home loan interest

Total deductions = ₹3,75,000

Taxable income = ₹11,25,000

Tax calculation:

- ₹0 – ₹2.5L → 0

- ₹2.5L – ₹5L → ₹12,500

- ₹5L – ₹10L → ₹1,00,000

- ₹10L – ₹11.25L → ₹37,500

Total tax = ₹1,50,000

Cess (4%) = ₹6,000

Final tax payable = ₹1,56,000

Verdict at ₹15L

New regime = ₹1,01,400

Old regime = ₹1,56,000

Even after solid deductions, new regime remains cheaper in this scenario.

So What’s the Final Answer on New vs Old Tax Regime 2026?

Here’s the simple takeaway:

- If your taxable income is up to ₹12 lakh → new regime effectively gives zero tax due to rebate.

- If you don’t aggressively maximize deductions → new regime usually wins.

- Old regime only makes sense if you have very high and structured deductions.

The biggest mistake?

Choosing emotionally instead of calculating.

When it comes to New vs Old Tax Regime 2026, don’t guess.

Run both numbers once.

The math doesn’t lie.

FAQs

Which is better in 2026 – new tax regime or old tax regime?

Under the New vs Old Tax Regime 2026 comparison, the new regime benefits most salaried individuals earning up to ₹12 lakh due to the Section 87A rebate. However, the old regime may be better if you have high deductions like home loan interest and full 80C usage.

Is tax zero under the new tax regime in 2026?

Yes, if your taxable income (after standard deduction) is up to ₹12 lakh, you can claim Section 87A rebate and reduce your tax liability to zero under the new regime.

Does the old tax regime still exist in 2026?

Yes, the old tax regime is still available. Taxpayers can choose between the new and old regime while filing income tax returns.

Can I switch between new and old tax regimes?

Salaried individuals can generally switch regimes every financial year while filing their return. However, business income cases may have restrictions.

Who should choose the old tax regime in 2026?

The old tax regime may be beneficial for individuals who:

Claim full 80C deductions

Have home loan interest

Claim HRA

Actively invest for tax savings

1 thought on “New vs Old Tax Regime 2026: Which One Saves More for Salaried People?”