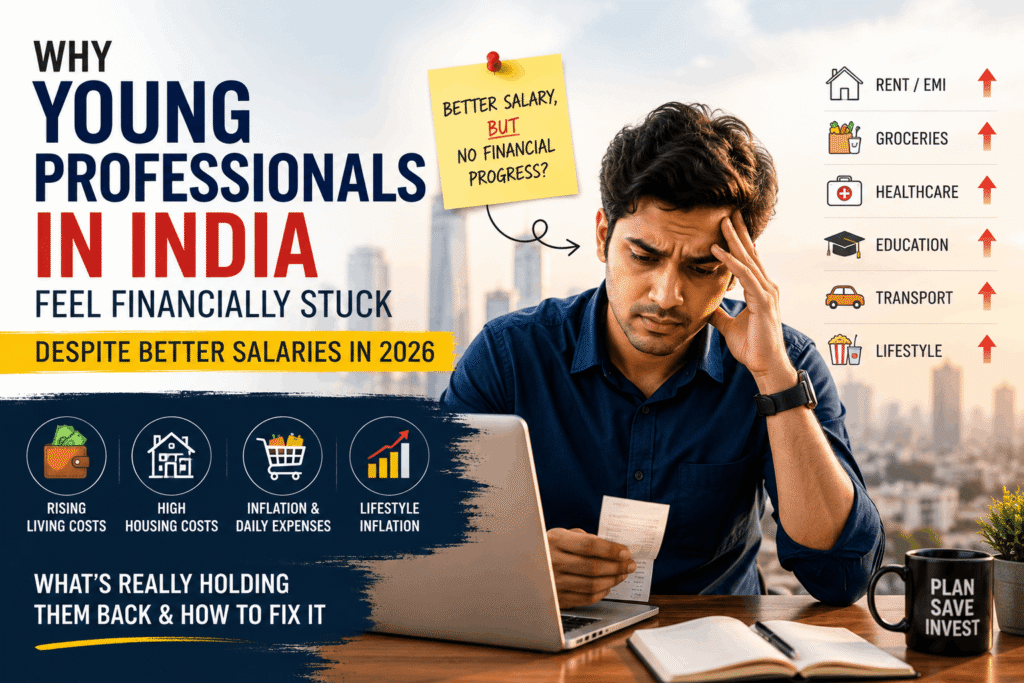

Landing a well-paying job is supposed to be a milestone. For many young professionals in India, however, a bigger paycheck no longer guarantees financial peace of mind.

A software engineer in Bengaluru, a banker in Mumbai, or an IT employee in Hyderabad may receive annual salary hikes but still wonder why their savings barely grow. Rent, EMIs, groceries, healthcare, and everyday bills seem to absorb every increase before the month is over.

If this sounds familiar, you are not alone.

The problem is not simply about earning more. It is about balancing a higher salary in India against rising living costs, inflation, and changing financial responsibilities.

According to the latest Consumer Price Index (CPI) data released by the Ministry of Statistics, India’s retail inflation rose to 3.93% in May 2026, up from 3.48% in April. The same release reported food inflation at 4.78%, with urban inflation at 3.53% and rural inflation at 4.25%.

Although inflation has eased compared with earlier highs, many essentials continue to consume a larger share of monthly income than they did a few years ago.

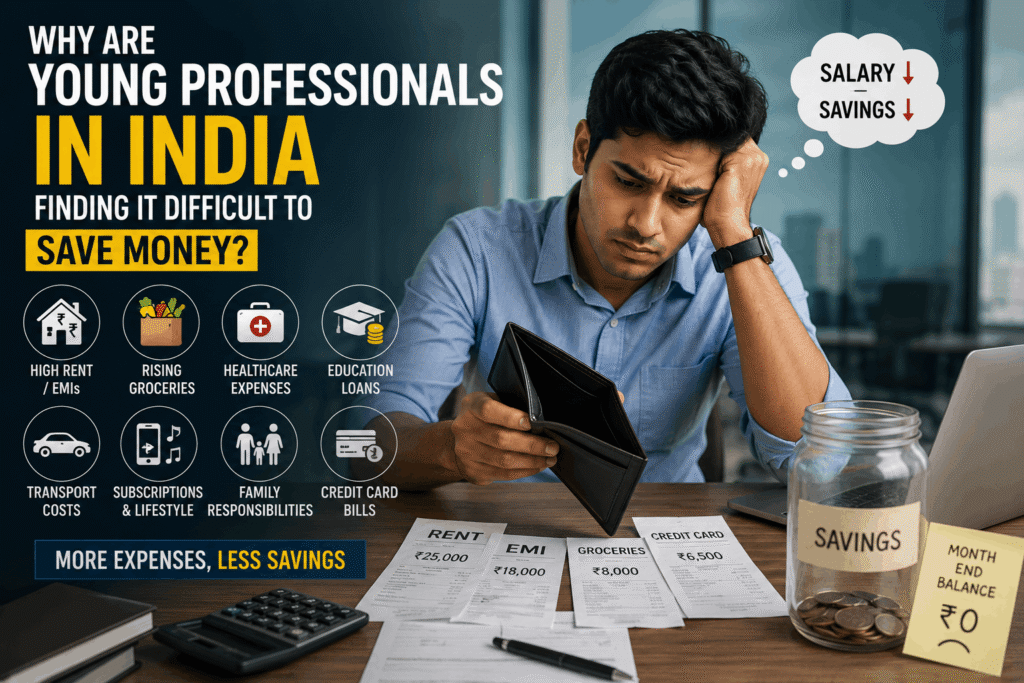

Why Are Young Professionals In India Finding It Difficult To Save Money?

Most young professionals begin their careers with clear financial goals. They want to buy a home, invest for the future, support their parents, travel, and enjoy a better lifestyle.

The reality often looks different.

A large part of every paycheck goes toward fixed expenses before any savings begin. Rent or home loan EMIs, groceries, electricity bills, fuel, internet, insurance, and mobile recharges quickly reduce disposable income.

Many professionals also manage education loans or contribute to family expenses, leaving less room to build emergency savings or invest consistently.

As incomes rise, responsibilities often rise as well.

Is Inflation In India The Only Reason?

Not entirely.

Inflation in India certainly affects purchasing power, but it is only one piece of the puzzle.

Housing costs, healthcare, education, transportation, and everyday services have all become more expensive. Even when headline inflation slows, households continue to feel pressure because several essential expenses increase at the same time.

If you want to understand this trend in greater detail, read our guide on the cost of living in India in 2026. It explains how rising housing costs, groceries, healthcare, and education are reshaping household budgets across the country.

Recent reporting from The Hindu’s Business and Economy section also highlights how inflation, food prices, and consumer spending continue to influence Indian households.

Why Doesn’t A Salary Hike Feel Like Real Progress?

The answer often lies in lifestyle inflation.

As income grows, spending tends to grow as well.

A promotion may encourage someone to rent a larger apartment. A salary hike may lead to a new smartphone, additional subscriptions, or more frequent dining out. These decisions are understandable, but together they increase monthly expenses.

Digital payments have made spending easier than ever. Apps such as PhonePe, Google Pay, and Paytm allow transactions to happen instantly, making it easy to overlook small purchases that gradually add up.

By the end of the month, many professionals discover that their higher salary has simply financed a more expensive lifestyle rather than increasing their wealth.

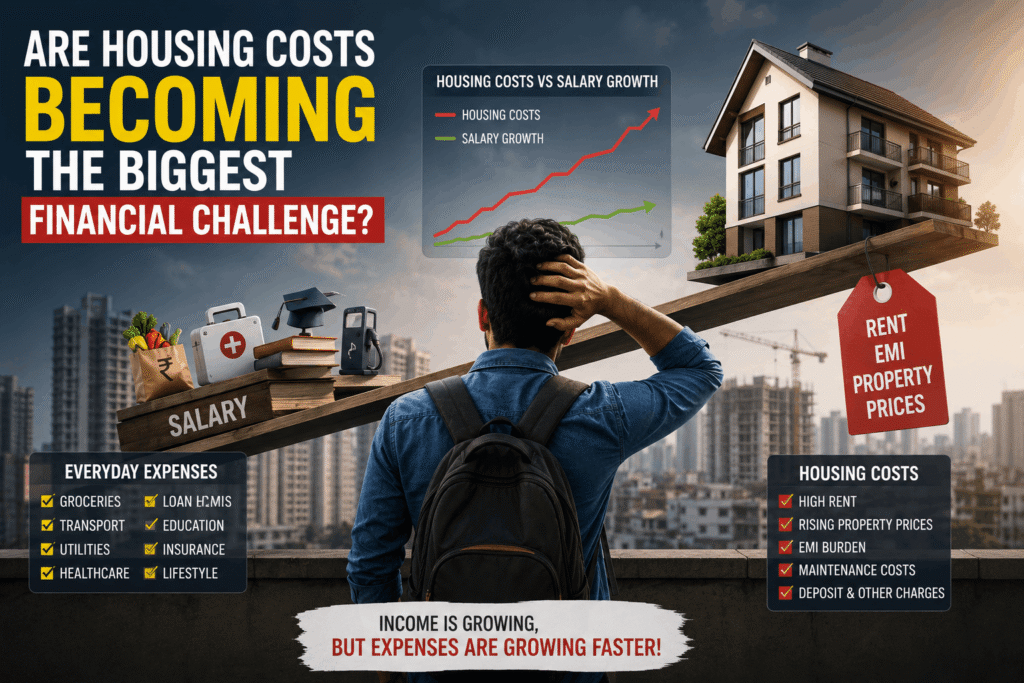

Are Housing Costs Becoming The Biggest Financial Challenge?

For many young Indians, housing is now the single largest monthly expense.

Cities like Bengaluru, Mumbai, Hyderabad, Pune, Chennai, and Gurugram continue to attract professionals because of better career opportunities. Strong demand for housing has contributed to higher rents across many of these employment hubs, although local market conditions vary from city to city.

Recent coverage from Moneycontrol’s real estate section continues to highlight sustained demand in India’s major property markets.

When a significant share of monthly income goes toward rent or home loan EMIs, saving becomes much more difficult. Once groceries, transportation, insurance, and utility bills are added, even a good salary can feel stretched.

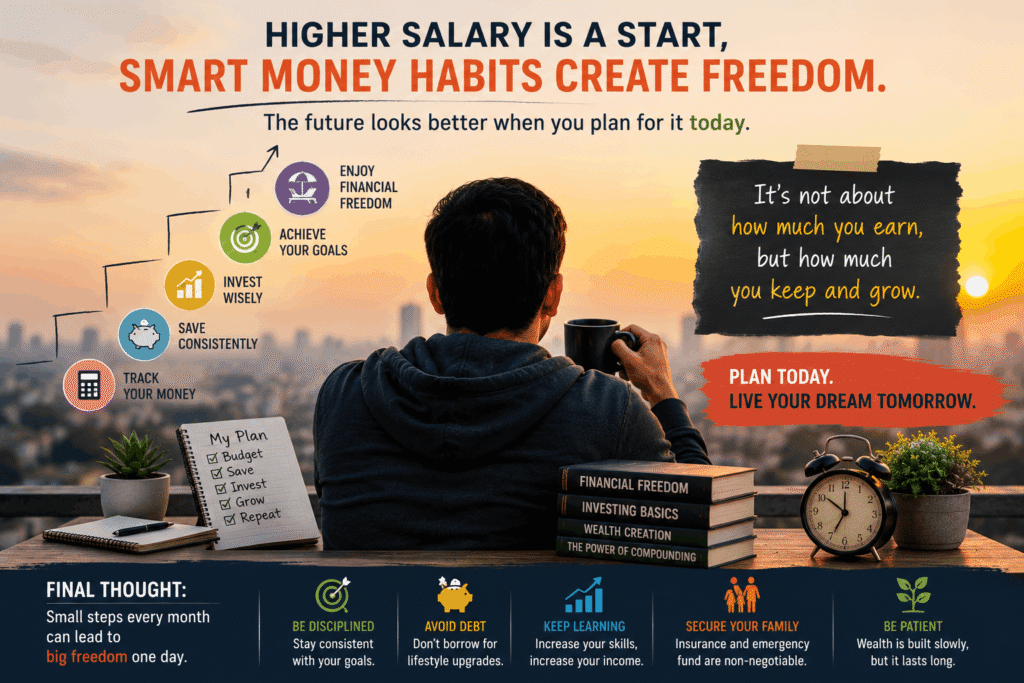

Why Is Financial Planning In India More Important Than Ever?

Earning more is only one part of financial success.

Managing money wisely has become equally important.

Today’s professionals often balance home loans, education loans, health insurance, investments, family responsibilities, and daily expenses all at the same time. Without a financial plan, it becomes easy to lose track of long-term goals.

According to the Reserve Bank of India’s latest monetary policy updates, maintaining price stability remains a key priority for supporting sustainable economic growth. However, every household experiences inflation differently depending on its spending habits and financial commitments.

Some simple habits can make a meaningful difference:

- Create a realistic monthly budget.

- Build an emergency fund covering several months of expenses.

- Increase SIP investments whenever your salary increases.

- Avoid unnecessary EMIs for lifestyle purchases.

- Review subscriptions and recurring expenses regularly.

- Track spending instead of relying on estimates.

These habits may not produce instant results, but they help create long-term financial stability.

The Bottom Line

Many young professionals in India are earning better salaries than previous generations.

Yet many still feel financially stuck.

The reason is not simply inflation in India. It is the combined effect of rising housing costs, healthcare expenses, education costs, lifestyle inflation, and changing financial expectations.

These same factors are also increasing the cost of living in India, making it harder for young professionals to turn higher salaries into lasting financial security.

A bigger paycheck is still valuable, but financial freedom depends on more than income alone.

For today’s generation, success is not just about earning more. It is about saving consistently, investing wisely, and making sure each salary increase improves the future instead of simply paying for a more expensive present.

FAQs

Why are young professionals in India struggling to save money?

Many young professionals in India face rising housing costs, healthcare expenses, education costs, and lifestyle inflation, making it difficult to save despite earning higher salaries.

Is inflation in India reducing purchasing power?

Yes. Inflation affects the cost of everyday essentials such as groceries, transportation, healthcare, and utilities, reducing the purchasing power of household income.

Why don’t salary hikes feel enough anymore?

Salary increases are often offset by rising living costs, higher rents, EMIs, and lifestyle inflation, leaving little room for additional savings.

How can young professionals in India improve their financial situation?

Creating a monthly budget, building an emergency fund, investing through SIPs, avoiding unnecessary debt, and tracking expenses can improve long-term financial health.

What is lifestyle inflation?

Lifestyle inflation happens when spending increases as income rises, reducing the benefits of salary growth and making it harder to build wealth.

Which Indian cities are the most expensive for young professionals?

Cities such as Bengaluru, Mumbai, Gurugram, Hyderabad, Pune, and Chennai generally have higher housing and living costs than many other parts of India.

Is financial planning important even with a good salary?

Yes. Financial planning helps young professionals manage expenses, prepare for emergencies, invest consistently, and achieve long-term financial goals.

How does the cost of living affect young professionals in India?

Rising housing, healthcare, education, transportation, and food costs leave many professionals with less disposable income, even after receiving salary hikes.

2 thoughts on “Why Young Indians Feel Financially Stuck Despite Better Salaries In 2026: What’s Really Holding Them Back”