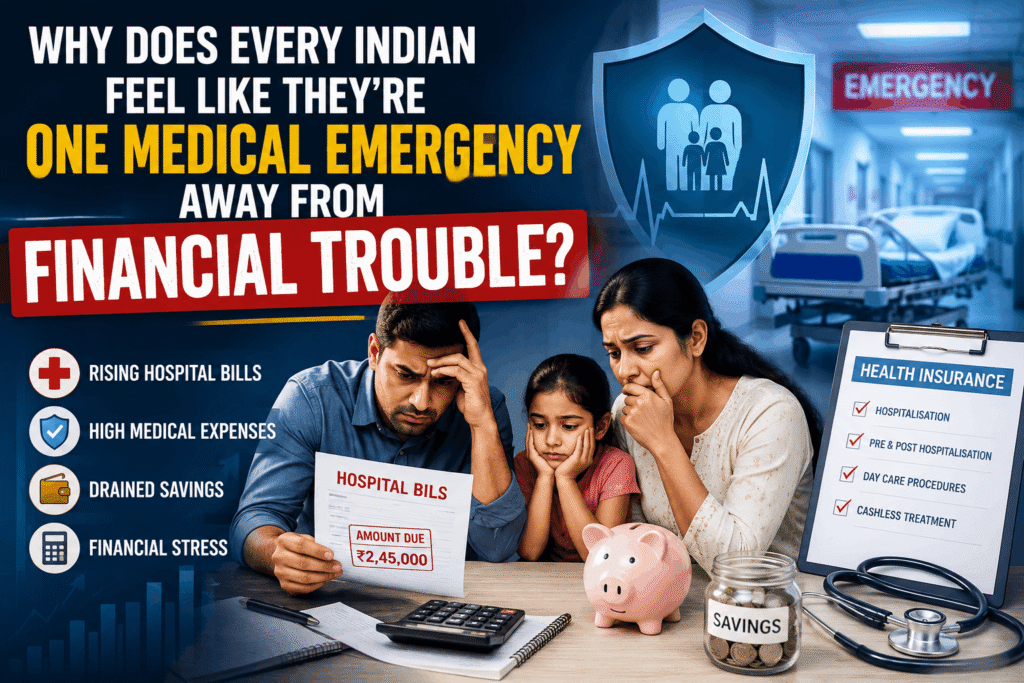

For many Indian families, the fear of falling sick is no longer just about health. It is about what the hospital bill could do to their finances.

A sudden accident, emergency surgery, or serious illness can wipe out years of savings within days. Even families with stable incomes often worry that one unexpected medical emergency could force them to dip into investments, take a personal loan, or delay important life goals.

That concern is becoming increasingly common because healthcare costs in India continue to rise while household budgets are already stretched by higher housing costs, education expenses, transportation, and everyday living costs.

According to the latest Consumer Price Index (CPI) data released by the Ministry of Statistics, India’s retail inflation rose to 3.93% in May 2026, up from 3.48% in April. The same official release reported food inflation at 4.78%, while urban retail inflation stood at 3.53% and rural inflation reached 4.25%. Although overall inflation has moderated compared with earlier highs, many essential household expenses continue to put pressure on family finances.

Healthcare is different from most other expenses because it rarely comes with advance notice.

Unlike rent or school fees, a medical emergency cannot be planned for. It arrives unexpectedly, often requiring immediate treatment and immediate financial decisions.

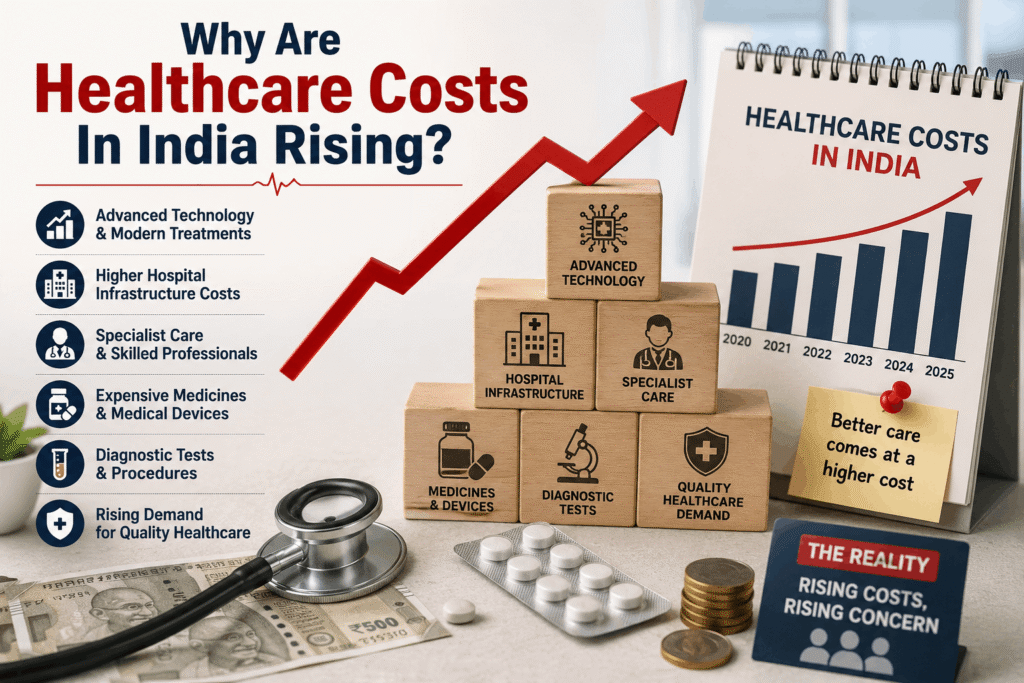

Why Are Healthcare Costs In India Rising?

Healthcare in India has improved significantly over the last decade.

Modern hospitals now offer advanced diagnostic technology, specialised treatments, minimally invasive procedures, and better emergency care than ever before. These improvements have helped save countless lives, but they have also increased the overall cost of treatment.

During a hospital admission, families are often paying for much more than the doctor’s consultation.

They may also face expenses for:

- Hospital room charges

- Diagnostic tests and scans

- Medicines

- Specialist consultations

- Medical equipment

- Follow-up treatment

- Rehabilitation and home care

When these expenses are combined, the final bill can be overwhelming for households that have not prepared financially.

Recent reporting from The Hindu’s Health section continues to highlight the importance of improving healthcare affordability and financial preparedness for Indian families.

Why Do Even Middle-Class Families Feel Financially Vulnerable?

Many people assume that financial hardship caused by medical emergencies affects only low-income households.

The reality is much broader.

A growing number of middle-class families are already balancing home loan EMIs, school fees, vehicle loans, household expenses, insurance premiums, retirement planning, and support for ageing parents.

When an unexpected hospital bill arrives, those carefully managed finances can quickly come under pressure.

This financial anxiety is not limited to older households. Our article on why young professionals in India are earning better salaries but still struggling financially explains how many younger workers also feel financially vulnerable despite salary growth. As careers progress and family responsibilities increase, that same pressure often follows people into middle age.

Those pressures become even more visible in our analysis of why middle-class Indians feel richer on paper but poorer in reality. Higher incomes often fail to create lasting financial security because housing, education, healthcare, and other essential expenses continue to rise.

The challenge is not always low income.

More often, it is the lack of financial flexibility when an emergency happens without warning.

Is Health Insurance India Enough To Protect Families?

For many households, health insurance India provides an essential layer of financial protection.

However, insurance is not always a complete solution.

Every policy has different coverage limits, waiting periods, exclusions, room rent caps, co-payment clauses, and claim conditions.

Some families only discover these limitations after they need to make a claim.

Others postpone buying insurance because they feel healthy or believe the premiums are an unnecessary expense.

Unfortunately, illnesses and accidents rarely give advance notice.

That is why financial experts consistently recommend purchasing adequate health insurance before it becomes necessary rather than after a health problem develops.

Recent coverage from Moneycontrol’s personal finance section also highlights growing awareness of health insurance, emergency savings, and long-term financial planning among Indian households.

How Do Medical Expenses In India Affect Everyday Families?

The financial impact often continues long after the patient leaves the hospital.

Recovery may require weeks away from work, additional medicines, follow-up consultations, physiotherapy, or home care.

In many cases, another family member also takes leave from work to provide support, reducing household income at the very moment expenses are increasing.

Consider a middle-class family living in Pune.

Both parents are employed, they are paying a home loan, and their child attends a private school.

An unexpected hospital bill running into several lakh rupees may not only reduce their savings but also delay investment plans, children’s education goals, or even the purchase of a new home.

Why Is Healthcare Affordability India Becoming A Bigger Concern?

The issue is no longer limited to hospital bills.

It is about whether ordinary families can manage healthcare expenses while also meeting every other financial responsibility.

Our detailed guide on the cost of living in India in 2026 explains how rising housing costs, groceries, education, transportation, and utility bills are already putting pressure on household budgets. When unexpected medical expenses are added to those existing commitments, many families quickly find themselves under severe financial strain.

For many Indians, the biggest concern is not whether quality healthcare is available.

It is whether they can afford it when they need it most.

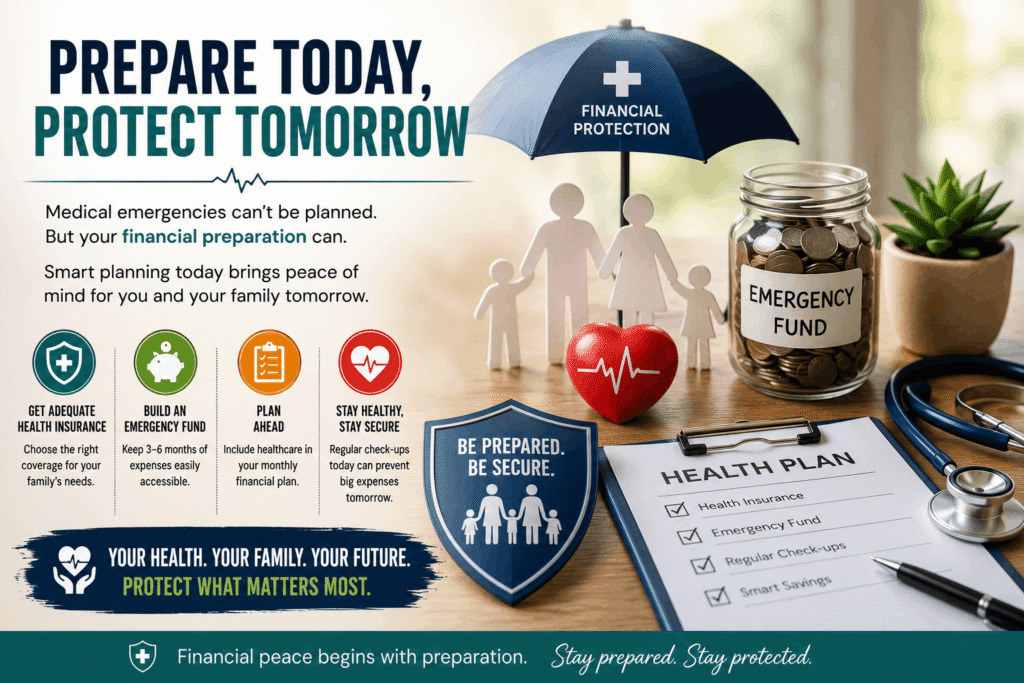

Can An Emergency Fund Really Protect Families?

Yes, and in many situations it becomes just as important as health insurance.

Insurance can reduce the financial burden of hospitalization, but it does not always cover every expense. Families may still have to pay for medicines outside the policy, follow-up consultations, rehabilitation, travel, home care, or temporary income loss if someone is unable to work.

That is why financial planners recommend building an emergency fund alongside adequate health insurance.

An emergency fund gives families immediate access to money without depending on credit cards, personal loans, or borrowing from relatives during a crisis.

Even setting aside a small amount every month can gradually create a financial cushion that provides peace of mind when unexpected situations arise.

Why Is Financial Planning Becoming Essential For Indian Families?

Medical emergencies are only one part of the financial challenges facing Indian households.

Most middle-class families are already managing home loan EMIs, school fees, grocery bills, insurance premiums, transportation costs, retirement planning, and everyday household expenses.

Without a clear financial plan, one unexpected hospital admission can disrupt years of careful budgeting.

According to the Reserve Bank of India’s latest monetary policy updates, maintaining price stability remains one of the central bank’s key priorities for supporting sustainable economic growth.

However, national inflation figures do not always reflect an individual household’s experience. Family responsibilities, housing costs, and healthcare expenses often create financial pressure that feels much greater than headline inflation suggests.

That is why financial planning has become one of the most valuable life skills for Indian families.

Recent reporting by The Economic Times on India’s economy and household finances also points to changing spending patterns, rising household costs, and the growing importance of emergency savings and long-term financial planning.

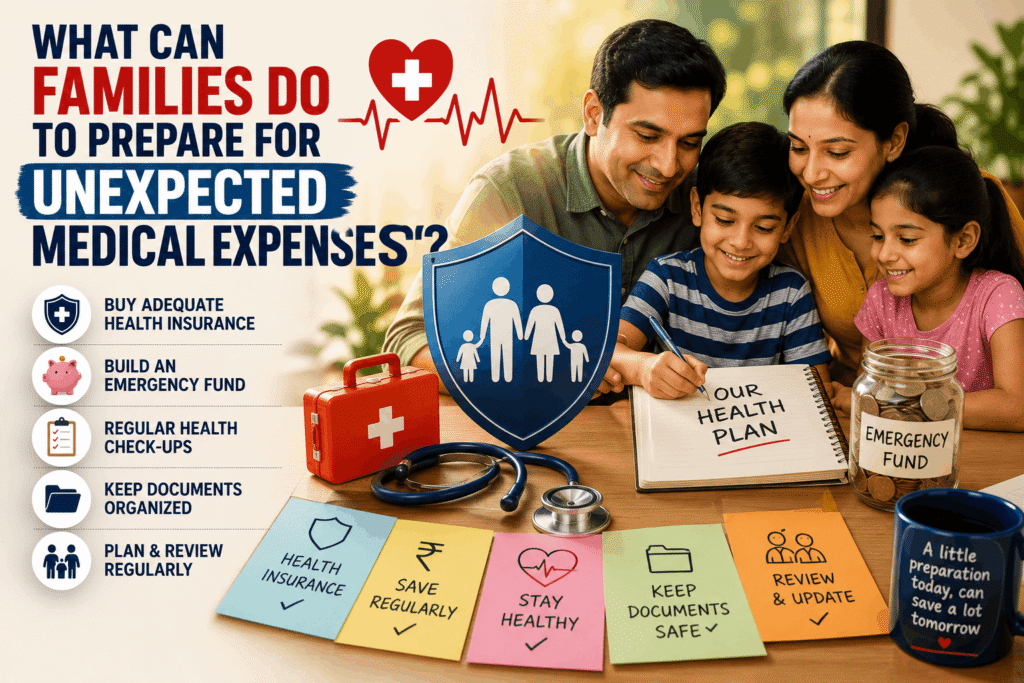

What Can Families Do To Prepare For Unexpected Medical Expenses?

No one can completely eliminate the risk of a medical emergency.

However, there are several practical steps families can take to reduce the financial impact.

- Choose a health insurance policy that matches your family’s healthcare needs instead of focusing only on the lowest premium.

- Build an emergency fund that can cover at least three to six months of essential household expenses.

- Review your insurance coverage every year as your family’s circumstances change.

- Keep important medical records and insurance documents organised and easily accessible.

- Schedule regular preventive health check-ups, as early diagnosis often reduces treatment costs.

- Include healthcare expenses in your monthly financial planning instead of treating them as unexpected costs.

These habits may seem simple, but together they can significantly reduce financial stress during a medical emergency.

Is The Fear Of Medical Emergencies Really About Money?

Money is certainly a major part of the concern.

However, uncertainty plays an equally important role.

No family can predict when an accident, surgery, or serious illness might happen. That uncertainty creates emotional stress long before any hospital bill arrives.

Many families also worry about how a medical emergency could affect their children’s education, retirement plans, home loan repayments, or long-term investments.

The financial consequences often continue long after treatment has ended.

For many households, the greatest fear is not the illness itself.

It is losing years of financial progress because of one unexpected event.

The Bottom Line

The rising healthcare costs in India have made medical emergencies one of the biggest financial concerns for millions of households.

Although hospitals now offer better technology, advanced treatments, and improved healthcare services, quality medical care has also become more expensive for many families.

Healthcare expenses no longer exist in isolation.

They are closely connected to rising housing costs, education fees, transportation expenses, insurance premiums, and the broader increase in everyday living costs.

These financial pressures are closely connected. Rising healthcare costs in India do not exist in isolation. They are part of a broader financial reality that includes the cost of living in India, the challenges facing young professionals in India, and the growing concerns explored in our article on why middle-class Indians feel richer on paper but poorer in reality. Together, these trends show why many households feel increasingly vulnerable even when their incomes continue to grow.

A medical emergency cannot always be prevented.

Financial preparation, however, is something every family can work toward.

The combination of adequate health insurance in India, a dedicated emergency fund, disciplined financial planning, and regular savings can help reduce both financial stress and uncertainty when unexpected health problems arise.

For many Indian families, the question is no longer whether a medical emergency might happen.

The more important question is whether they are financially prepared if it does.

FAQs

Why are healthcare costs in India increasing?

Healthcare costs in India have increased due to higher treatment costs, advanced medical technology, specialist care, hospital infrastructure, medicines, and rising demand for quality healthcare services.

Can one medical emergency cause financial problems?

Yes. A major hospitalisation can create significant financial pressure, especially for families without adequate health insurance or emergency savings.

Is health insurance enough to cover all medical expenses?

Not always. Many policies have exclusions, waiting periods, co-payments, room rent limits, and coverage caps. Families should review their policy carefully and maintain an emergency fund for uncovered expenses.

How much emergency savings should Indian families keep?

Financial planners generally recommend maintaining an emergency fund covering at least three to six months of essential household expenses, alongside adequate health insurance.

Why do middle-class families worry about medical emergencies?

Many middle-class families already manage home loan EMIs, education costs, insurance premiums, and daily household expenses. A sudden hospital bill can disrupt savings and long-term financial plans.